.JPG)

Fecha: 24 de Mayo 2010

Fuente: http://www.infoweek.biz/la/2010/05/e-commerce-crece-a-tasas-de-dos-digitos/

Fecha: 24 de Mayo 2010

Fuente: http://www.infoweek.biz/la/2010/05/e-commerce-crece-a-tasas-de-dos-digitos/

Comentario:

Comentario:

By Conrad Sheehan

By Conrad SheehanThe Web is exploding with low-ticket items -- think 99-cent download for an MP3 -- but credit cards struggle at this price point, because they can't make money on purchases below $1 and also can't effectively manage the risk. What's needed is a payment network that is easy, convenient and secure for consumers to use while also simple and cost-effective for merchants to accept.

Forecasts for the magnitude of online micro-payments can whet the appetite of any profit-minded businessperson. However, cracking that code is more complicated than one thinks. There is little question as to whether sub-US$5 products can be sold in mass volume, but the lynchpin to opening the floodgates of micro-payments may very well be payment method.

Micro-payment business models work, and they work profitably. Some of the largest fortunes in America have been built on sales through micro-payments. Mars Corporation, Coca-Cola and Wrigley (I can glimpse the top of the Wrigley building if I lean "just so" out my office window) all made their fortunes selling goods at prices that can be la

beled "micro."

While vending and soda machines represent an automated micro-payment model, the question of whether micro-payments will work online is an altogether different one.

For one thing, online sales of physical items require shipping and handling that dwarfs the payment for the actual product and, consequently, limits micro-payments principally to the realm of digital content.

Apple, and specifically iTunes, is often held out as the archetype of a successful micro-payments business on the Web. It certainly is successful, but in order to reap the benefit of the micro-payment song purchase, customers likely have made a macro-payment to Apple for an iPod, iPod touch, iPhone -- or, less often, Apple TV.

In other words, Apple is not a pure-play, m

icro-payment business model but it does demonstrate, with

certainty, consumer demand for micro-purchases on the Web.

To get more insight into how a micro-payment business model might work on the Web, it is helpful to examine how the concept works in traditional brick-and-mortar commerce.

In brick-and-mortar stores, micro-payment businesses work

well even when the costs of goods sold are high due to raw materials, manufacturing, distribution, inventory, wholesaling and retailing. Some even self-identify

as micro-payment businesses, e.g., dollar stores.

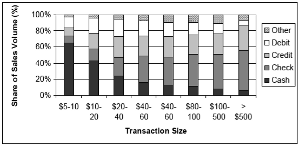

Common characteristics of micro-payment retail ![]() sales:

sales:

It is interesting to examine the relationship between micro-payments and the fact that they are paid for with cash.

We can safely conclude that consumers want and do make micro-purchases, online and offline, and that micro-payment business models are very sensitive to convenience and cost of processing. An exception to that rule exists for royalty-free digital content with zero variable costs, like virtual poker chips or digital sushi, for which the cost of payment is less critical.

Card-based solutions are neither convenient nor cost-effective for micro-purchases. PayPal or Google (Nasdaq: GOOG) Checkout, by storing credit card information under email and password credentials, address the convenience of purchase, but both struggle on the cost side. PayPal is largely credit-card based, and Google Checkout is all card-based.

Efforts in the past to address the costs of card processing of micro-payments by aggregating transactions into a single batch have not been successful. Other efforts to jury-rig credit cards for micro-payments include forcing the customer to purchase "credits" in round increments like $20. Pre-selling credits creates a stored value and closed-loop payment system, akin to the gift cards sold at grocery line checkout or in mass transit ticketing, where the funds may be used only with a single merchant.

Closed-loop systems are annoying for the customer, requiring another username/password combination. Further, residual balances are scattered all over the place. On the merchant side, closed-loop systems create accounting, data security and potentially escheatment issues -- i.e., unclaimed balances. Proprietary stored value systems are also expensive to maintain and operate, either eroding merchant margins or inhibiting consumer adoption due to fees passed on to them.

So, card-based solutions have not solved the problem -- not due to a lack of effort, but rather because the economics are just not there. Closed-loop systems try to address the economics but create other problems, the most critical of which is customer hassle.

What is absent is a payment network that is easy, convenient and secure for consumers to use while also simple and cost-effective for merchants to accept.

Electronic checks, which settle using the Automated Clearing House ("ACH"), hold potential because ACH is a very low-cost settlement system. However, the problem with ACH is that it is just a settlement system, not a complete payment solution. It began in the early 1970s, batch processing payroll and installment loan payments. Unfortunately, little has changed since in terms of capability.

Electronic checks are hard for consumers to access without an intermediary, and there are fraud and other financial risks within the ACH system that make it difficult or inadequate for a merchant to accept as a form of payment.

The diagram below frames payments systems along the key elements of cost and acceptance architecture. It makes clear the lack of options that are both open-loop and low-cost, and it explains the longstanding interest in and frustration with micropayments.

For all merchants -- both online and brick-and-mortar -- an electronic micro-payment solution must be based on the ACH system at its core, with as few intermediating layers as possible.

ACH alone, however, is inadequate. The solution will need to add

ress the structural gaps in ACH around fraud and financial risk. The solution will need to seamlessly enable a wide array of payment types -- including purchase, bill payments, recurring/subscription, international and person-to-person -- without sacrificing security and ease-of-use for all parties in the transaction.

The payment solution will also provide a balanced set of consumer and merchant protections, effective reporting, prompt settlement and scalability. Further, the solution will need to be available across multiple channels -- online, mobile, video game consoles, and any other emerging points of connectivity.

With just such a solution, digital content providers and other micro-payment merchants can go a long way toward capturing more revenue and value for their products and services.

Comentario: A través de aplicaciones como la que se destaca en esta noticia, vemos que m-commerce ha sido capaz de generar una ventaja competitiva para las empresas que fomentan su uso y dan un servicio que aporta mucho a los usuarios al disponer de la información que necesitan en cualquier parte. Así, este caso es uno de muchos mas que describe el gran valor que tienen hoy en día aplicaciones mòbiles en Chile y el mundo.

Comentario: A través de aplicaciones como la que se destaca en esta noticia, vemos que m-commerce ha sido capaz de generar una ventaja competitiva para las empresas que fomentan su uso y dan un servicio que aporta mucho a los usuarios al disponer de la información que necesitan en cualquier parte. Así, este caso es uno de muchos mas que describe el gran valor que tienen hoy en día aplicaciones mòbiles en Chile y el mundo.  Comentario:

Comentario:

Según Servent en estas negociaciones definirán el carácter de exclusividad que puede tener una empresa de telecomunicaciones determinada pero no quiso aportar mayores antecedentes para no perjudicar las mismas.

La empresa cerró recientemente una alianza con la cadena de cines CineHoyts, una de las principales cadenas de cines en Chile, destinada a promover la venta remota de boletos a través de plataformas tecnológicas, tales como call center y comercio electrónico empleando en este último caso el sistema Webpay provisto por el emisor de tarjetas de crédito Transbank.

Entradas Al Tiro es una empresa filial de DPS Automation, firma especializada en automatización de procesos, desarrollo de software e integración de tecnologías en Sudamérica. La empresa además está evaluando replicar este modelo en Brasil y Argentina.

Publicada: Viernes 09, Agosto 2002 19:56. Por Claudio Ramirez / Business News Americas

SANTIAGO

Si bien hace varios años que los cursos de inglés se habían alejado de las salas de clases, con lecciones por Internet o en DVD, ahora un novedoso formato se suma a la ya amplia oferta. Se trata de la primera iniciativa en Chile que busca enseñar este idioma a través del celular.

El objetivo es que con sólo bajar una aplicación, que pesa menos de 700 Kb, y cuya primera clase es gratuita, los usuarios de Movistar –la única empresa en el país que ofrece el servicio- puedan aprender el idioma, a través de 32 lecciones multimedia que comprenden escritura, e interacción con imágenes y audio.

Para probarlo sin costo alguno hay que enviar un mensaje de texto que diga "ingles" al 7272 y tras recibir un SMS, descargar la aplicación según el link indicado, transferencia que también es gratuita.

Desde la segunda lección en adelante el costo que se deberá pagar es de 990 pesos chilenos por clase, aunque también se pueden comprar paquetes de cuatro lecciones a un precio más rebajado.

Si tras bajar la prueba gratis se compra una segunda clase, el servicio ofrecerá primero un test para evaluar el nivel de inglés que el usuario posee, tras lo cual las clases se adaptarán a su manejo del idioma, guiando al usuario con sencillas instrucciones en español.

En total son cuatro niveles, compuestos de 8 unidades cada uno, que abordan diferentes temas como trabajo, familia, compras, comida, viajes, entre otros. A su vez, cada unidad contiene ocho lecciones, para un total de 256 actividades de aprendizaje.

Actualmente las aplicaciones son compatibles con 50 de los teléfonos más empleados por los clientes de Movistar, de fabricantes como SonyEriccson, Nokia y Motorola, lo que en total significa que puede ser empleadas por cerca de 500 mil personas. Por ahora no funciona con ningún BlackBerry ni tampoco con el iPhone, porque en este dispositivo las aplicaciones se comprar sólo a través de una tienda de Apple, sin que intermedie la compañía de teléfonos.

No obstante, el desarrollador de la aplicación, Kantoo English, aseguró que en tres semanas más el curso estará disponible para los diferentes modelos de Blackberry.

Venezuela fue el primer país de América Latina donde se lanzó Kantoo English, con más de 42 mil usuarios en los primeros tres meses, de los cuales un 94% destacó al programa como "un muy buen método para aprender inglés". Asímismo, un sondeo piloto en cinco ciudades de este país, a personas que usaron la aplicación, reveló que el 87% estarían dispuestos a recomendarla, sobre todo por su facilidad de uso y la posibilidad de adaptar el estudio con el horario de cada persona.

Por su parte, Helit Maiman, presidenta del directorio de La Mark, empresa que desarrolló Kantoo, dijo que "hemos reunido a un equipo de expertos de diferentes lugares del mundo, entre quienes se encuentran lingüistas, pedagogos, expertos en innovación, en tecnología inalámbrica, y en pruebas para usuarios, para lanzar este programa con la finalidad de que aprender y practicar inglés sea accesible para todos en cualquier parte".

comentario: el uso cotidiano del celular ha dado paso a nuevos negocios, como es el M-commerce, siento que este servicio de curso de ingles, es un claro ejemplo de la variedad de servicios que puede ofrecer esta tecnologia, ademas tiene un excelente gancho comercial, que las primeras clases de ingles sean gratuitas, y de esta menera tomar la decision de seguir con el servicio o no.